Then the bootstrap error distribution approximates the sampling distribution \[(\tilde{t}_i - \hat{t}) \overset{\mathcal{D}}{\sim} \hat{t} - t_0\]

The Non-Parametric Bootstrap

The non-parametric bootstrap is the most “naive” approach to the bootstrap: resample-then-estimate.

Non-Parametric Bootstrap

Why Use The Bootstrap?

Do not need to rely on variance asymptotics;

Can obtain non-symmetric CIs.

Approaches to Bootstrapping Structured Data

Correlations: Transform to uncorrelated data (principal components, etc.), sample, transform back.

Time Series: Block bootstrap

Generalizing the Block Bootstrap

The rough transitions in the block bootstrap can really degrade estimator quality.

Improve transitions between blocks

Moving blocks (allow overlaps)

Sources of Non-Parametric Bootstrap Error

Sampling error: error from using finitely many replications

Statistical error: error in the bootstrap sampling distribution approximation

When To Use The Non-Parametric Bootstrap

Sample is representative of the data distribution

Doesn’t work well for extreme values!

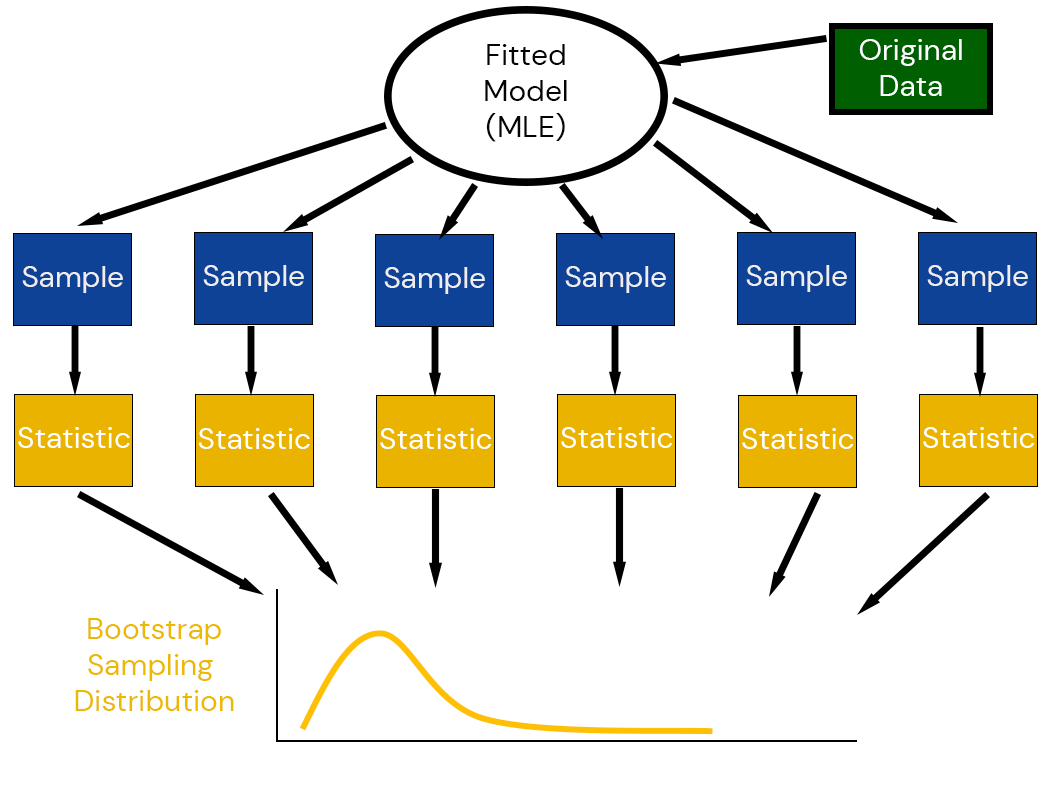

The Parametric Bootstrap

The Parametric Bootstrap

Non-Parametric Bootstrap: Resample directly from the data.

Parametric Bootstrap: Fit a model to the original data and simulate new samples, then calculate bootstrap estimates.

This lets us use additional information, such as a simulation or statistical model.

Parametric Bootstrap Scheme

The parametric bootstrap generates pseudodata using fitted model simulations.

Parametric Bootstrap

Benefits of the Parametric Bootstrap

Can quantify uncertainties in parameter values

Deals better with structured data (model accounts for structure)

Potential Drawbacks

New source of error: model specification

Misspecified models can completely distort estimates.

Example: 100-Year Return Periods

Detrended San Francisco Tide Gauge Data:

Code

# read in data and get annual maximafunctionload_data(fname) date_format =DateFormat("yyyy-mm-dd HH:MM:SS")# This uses the DataFramesMeta.jl package, which makes it easy to string together commands to load and process data df =@chain fname begin CSV.read(DataFrame; header=false)rename("Column1"=>"year", "Column2"=>"month", "Column3"=>"day", "Column4"=>"hour", "Column5"=>"gauge")# need to reformat the decimal date in the data file@transform:datetime =DateTime.(:year, :month, :day, :hour)# replace -99999 with missing@transform:gauge =ifelse.(abs.(:gauge) .>=9999, missing, :gauge)select(:datetime, :gauge)endreturn dfenddat =load_data("data/surge/h551.csv")# detrend the data to remove the effects of sea-level rise and seasonal dynamicsma_length =366ma_offset =Int(floor(ma_length/2))moving_average(series,n) = [mean(@view series[i-n:i+n]) for i in n+1:length(series)-n]dat_ma =DataFrame(datetime=dat.datetime[ma_offset+1:end-ma_offset], residual=dat.gauge[ma_offset+1:end-ma_offset] .-moving_average(dat.gauge, ma_offset))# group data by year and compute the annual maximadat_ma =dropmissing(dat_ma) # drop missing datadat_annmax =combine(dat_ma -> dat_ma[argmax(dat_ma.residual), :], groupby(transform(dat_ma, :datetime =>x->year.(x)), :datetime_function))delete!(dat_annmax, nrow(dat_annmax)) # delete 2023; haven't seen much of that year yetrename!(dat_annmax, :datetime_function =>:Year)select!(dat_annmax, [:Year, :residual])dat_annmax.residual = dat_annmax.residual /1000# convert to m# make plotsp1 =plot( dat_annmax.Year, dat_annmax.residual; xlabel="Year", ylabel="Annual Max Tide (m)", label=false, marker=:circle, markersize=5, tickfontsize=16, guidefontsize=18)p2 =histogram( dat_annmax.residual, normalize=:pdf, orientation=:horizontal, label=:false, xlabel="PDF", ylabel="", yticks=[], tickfontsize=16, guidefontsize=18)l =@layout [a{0.7w} b{0.3w}]plot(p1, p2; layout=l, link=:y, ylims=(1, 1.7), bottom_margin=10mm, left_margin=5mm)plot!(size=(1000, 350))

Figure 1: Annual maxima surge data from the San Francisco, CA tide gauge.

Parametric Bootstrap Strategy

Fit GEV Model

Compute 0.99 Quantile

Repeat \(N\) times:

Resample Extreme Values from GEV

Calculate 0.99 quantile.

Compute Confidence Intervals

Parametric Bootstrap Results

Code

# function to fit GEV model for each data setinit_θ = [1.0, 1.0, 1.0]gev_lik(θ) =-sum(logpdf(GeneralizedExtremeValue(θ[1], θ[2], θ[3]), dat_annmax.residual))# get estimates from observationsrp_emp =quantile(dat_annmax.residual, 0.99)θ_mle = Optim.optimize(gev_lik, init_θ).minimizerp =histogram(dat_annmax.residual, normalize=:pdf, xlabel="Annual Maximum Storm Tide (m)", ylabel="Probability Density", tickfontsize=16, guidefontsize=18, label=false, right_margin=5mm, bottom_margin=5mm, legendfontsize=18, left_margin=5mm)plot!(p, GeneralizedExtremeValue(θ_mle[1], θ_mle[2], θ_mle[3]), linewidth=3, label="Parametric Model")vline!(p, [rp_emp], color=:red, linewidth=3, linestyle=:dash, label="Empirical Return Level")xlims!(p ,0, 2)

Rahmstorf, S., & Coumou, D. (2011). Increase of extreme events in a warming world. Proceedings of the National Academy of Sciences, 108, 17905–17909. https://doi.org/10.1073/pnas.1101766108